Page 12 - LN DISSOLUTION OF FIRM

P. 12

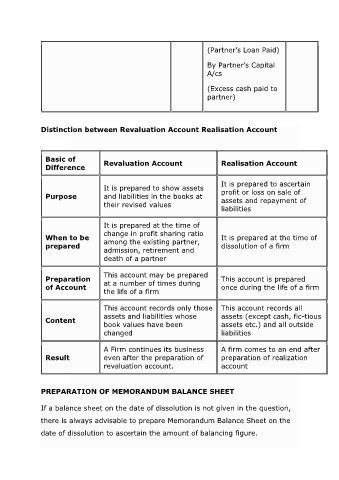

(Partner’s Loan Paid)

By Partner’s Capital

A/cs

(Excess cash paid to

partner)

Distinction between Revaluation Account Realisation Account

Basic of

Difference Revaluation Account Realisation Account

It is prepared to ascertain

It is prepared to show assets profit or loss on sale of

Purpose and liabilities in the books at assets and repayment of

their revised values

liabilities

It is prepared at the time of

change in profit sharing ratio

When to be It is prepared at the time of

prepared among the existing partner, dissolution of a firm

admission, retirement and

death of a partner

This account may be prepared

Preparation at a number of times during This account is prepared

of Account once during the life of a firm

the life of a firm

This account records only those This account records all

assets and liabilities whose assets (except cash, fic-tious

Content

book values have been assets etc.) and all outside

changed liabilities

A Firm continues its business A firm comes to an end after

Result even after the preparation of preparation of realization

revaluation account. account

PREPARATION OF MEMORANDUM BALANCE SHEET

If a balance sheet on the date of dissolution is not given in the question,

there is always advisable to prepare Memorandum Balance Sheet on the

date of dissolution to ascertain the amount of balancing figure.