Page 11 - LN DISSOLUTION OF FIRM

P. 11

By Cash/Bank A/c Cash

brought in

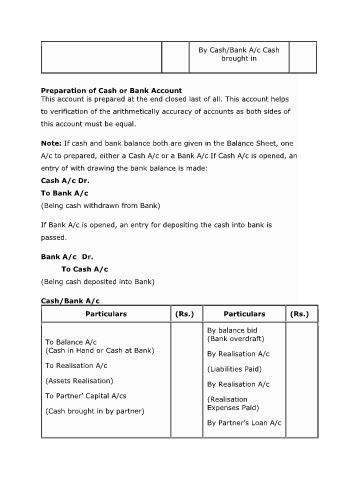

Preparation of Cash or Bank Account

This account is prepared at the end closed last of all. This account helps

to verification of the arithmetically accuracy of accounts as both sides of

this account must be equal.

Note: If cash and bank balance both are given in the Balance Sheet, one

A/c to prepared, either a Cash A/c or a Bank A/c If Cash A/c is opened, an

entry of with drawing the bank balance is made:

Cash A/c Dr.

To Bank A/c

(Being cash withdrawn from Bank)

If Bank A/c is opened, an entry for depositing the cash into bank is

passed.

Bank A/c Dr.

To Cash A/c

(Being cash deposited into Bank)

Cash/Bank A/c

Particulars (Rs.) Particulars (Rs.)

By balance bid

To Balance A/c (Bank overdraft)

(Cash in Hand or Cash at Bank) By Realisation A/c

To Realisation A/c (Liabilities Paid)

(Assets Realisation) By Realisation A/c

To Partner’ Capital A/cs (Realisation

(Cash brought in by partner) Expenses Paid)

By Partner’s Loan A/c