Page 3 - LESSON NOTE

P. 3

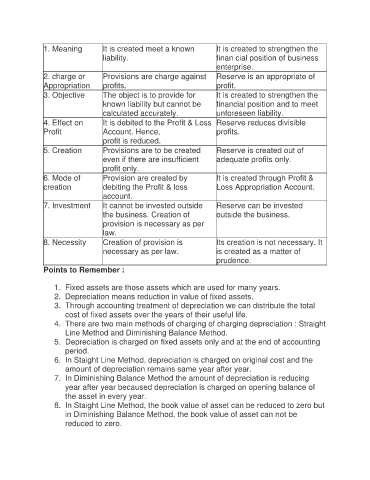

1. Meaning It is created meet a known It is created to strengthen the

liability. finan cial position of business

enterprise.

2. charge or Provisions are charge against Reserve is an appropriate of

Appropriation profits. profit.

3. Objective The object is to provide for It is created to strengthen the

known liability but cannot be financial position and to meet

calculated accurately. unforeseen liability.

4. Effect on It is debited to the Profit & Loss Reserve reduces divisible

Profit Account. Hence, profits.

profit is reduced.

5. Creation Provisions are to be created Reserve is created out of

even if there are insufficient adequate profits only.

profit only.

6. Mode of Provision are created by It is created through Profit &

creation debiting the Profit & loss Loss Appropriation Account.

account.

7. Investment It cannot be invested outside Reserve can be invested

the business. Creation of outside the business.

provision is necessary as per

law.

8. Necessity Creation of provision is Its creation is not necessary. It

necessary as per law. is created as a matter of

prudence.

Points to Remember :

1. Fixed assets are those assets which are used for many years.

2. Depreciation means reduction in value of fixed assets.

3. Through accounting treatment of depreciation we can distribute the total

cost of fixed assets over the years of their useful life.

4. There are two main methods of charging of charging depreciation : Straight

Line Method and Diminishing Balance Method.

5. Depreciation is charged on fixed assets only and at the end of accounting

period.

6. In Staight Line Method, depreciation is charged on original cost and the

amount of depreciation remains same year after year.

7. In Diminishing Balance Method the amount of depreciation is reducing

year after year becaused depreciation is charged on opening balance of

the asset in every year.

8. In Staight Line Method, the book value of asset can be reduced to zero but

in Diminishing Balance Method, the book value of asset can not be

reduced to zero.