Page 4 - Lesson Note

P. 4

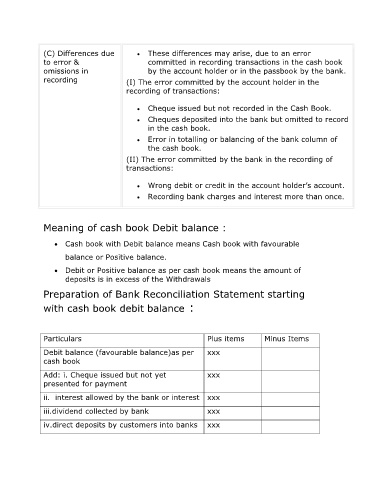

(C) Differences due These differences may arise, due to an error

to error & committed in recording transactions in the cash book

omissions in by the account holder or in the passbook by the bank.

recording (I) The error committed by the account holder in the

recording of transactions:

Cheque issued but not recorded in the Cash Book.

Cheques deposited into the bank but omitted to record

in the cash book.

Error in totalling or balancing of the bank column of

the cash book.

(II) The error committed by the bank in the recording of

transactions:

Wrong debit or credit in the account holder’s account.

Recording bank charges and interest more than once.

Meaning of cash book Debit balance :

Cash book with Debit balance means Cash book with favourable

balance or Positive balance.

Debit or Positive balance as per cash book means the amount of

deposits is in excess of the Withdrawals

Preparation of Bank Reconciliation Statement starting

with cash book debit balance :

Particulars Plus items Minus Items

Debit balance (favourable balance)as per xxx

cash book

Add: i. Cheque issued but not yet xxx

presented for payment

ii. interest allowed by the bank or interest xxx

iii.dividend collected by bank xxx

iv.direct deposits by customers into banks xxx