Page 3 - LN

P. 3

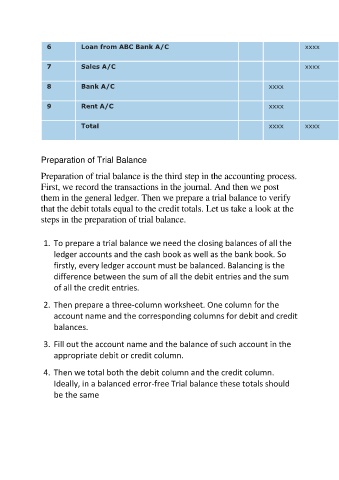

6 Loan from ABC Bank A/C xxxx

7 Sales A/C xxxx

8 Bank A/C xxxx

9 Rent A/C xxxx

Total xxxx xxxx

Preparation of Trial Balance

Preparation of trial balance is the third step in the accounting process.

First, we record the transactions in the journal. And then we post

them in the general ledger. Then we prepare a trial balance to verify

that the debit totals equal to the credit totals. Let us take a look at the

steps in the preparation of trial balance.

1. To prepare a trial balance we need the closing balances of all the

ledger accounts and the cash book as well as the bank book. So

firstly, every ledger account must be balanced. Balancing is the

difference between the sum of all the debit entries and the sum

of all the credit entries.

2. Then prepare a three-column worksheet. One column for the

account name and the corresponding columns for debit and credit

balances.

3. Fill out the account name and the balance of such account in the

appropriate debit or credit column.

4. Then we total both the debit column and the credit column.

Ideally, in a balanced error-free Trial balance these totals should

be the same